Think of your home as a ship. It sails through the sea of life, which can sometimes get stormy. Home insurance is like an anchor for your ship. It keeps your home safe, especially when bad weather hits. Bad weather can cause a lot of damage to our homes. But, with home insurance, you don’t need to worry. It protects your homes from these damages. In this article, we will learn more about how home insurance protects us from weather-related damages.

Table of Contents:

Basics of Home Insurance

Home insurance is like a safety net for your home. It’s a type of insurance policy that covers your home and the items inside it. If something bad happens, like a fire or a theft, home insurance can help you cover the costs.

There are different types of home insurance policies. Each one offers a different level of protection. Some policies only cover the structure of your home. Others also cover the items inside your home, like your furniture and electronics. Here is a quick look at the types of home insurance:

- HO-1: Basic Form: Include fire or lightning, windstorm or hail, vandalism or malicious mischief, theft, damage from vehicles and aircraft etc.

- HO-2: Broad Form: Same as HO-1 but it has some additional perils like it includes falling objects; weight of ice, snow, or sleet; accidental discharge or overflow of water or steam etc.

- HO-3: Special Form: The policy provides complete coverage for your home and structures, with exclusions listed.

- HO-4: Renters Insurance: The HO-4 policy provides coverage for a renter’s personal property and liability against the same perils as the HO-2 policy.

- HO-5: Comprehensive Form: The HO-5 insurance policy provides more extensive coverage than the HO-3 and is usually more costly. It is commonly utilized for upscale residences and personal belongings.

- HO-6: Condo Insurance: Coverage for both the portion of the building that you own and all the personal belongings that you store inside it.

To read in more detail about Home insurance and Types: “Home Insurance Works & Its Types”

ICICI Bharat Griha Raksha Policy – Home Insurance

One important thing to know is that many home insurance policies cover weather-related damage. If a storm damages your roof or a tree falls on your house, your insurance can help you pay for the repairs. This is a standard part of most home insurance policies.

Weather-Related Damages Covered by Home Insurance

Now, we have comprehended the significance of home insurance and its different types. Let’s explore the different types of weather-related damages that are usually covered by home insurance.

- Wind Damage: Wind can be a powerful force, capable of knocking down trees and causing significant damage to your home. Home insurance typically covers wind damage, including damage caused by fallen trees.

- Hail Damage: Hailstones can cause considerable damage to the exterior of your home, including your roof and siding. Most home insurance policies cover hail damage.

- Snow Damage: Heavy snowfall can lead to a variety of problems, including roof collapse. If a winter storm causes your roof to cave in under the weight of the snow, your home insurance policy will likely cover the damage.

- Water Damage: While home insurance typically covers water damage, it’s important to note that this doesn’t include floods. If a storm causes a leak in your roof leading to water damage inside your home, your insurance will likely cover it.

- Lightning Strikes and Power Surges: If a lightning strike causes a fire or a power surge that damages your electronics, your home insurance policy should cover the damage.

- Wildfires: In areas prone to wildfires, home insurance policies typically provide coverage for damage caused by fire.

- Damage from Falling Objects: This could include damage from objects like branches or even entire trees falling on your home during a storm.

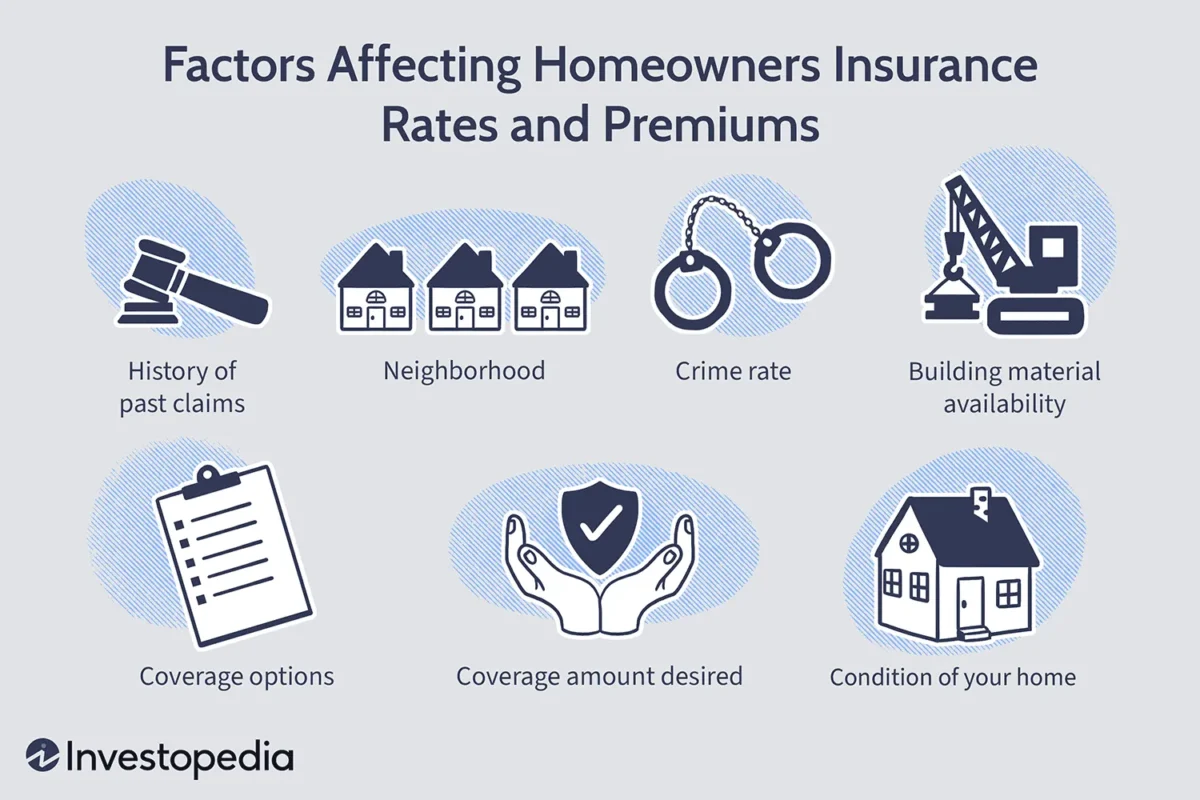

Remember, the exact coverage can vary depending on your specific policy and insurance provider. It’s important to know that the protection you get from your insurance policy might be different from someone else’s, depending on the policy and the insurance company.

Some things might not be covered unless you pay extra money for more protection. For example, if your house gets damaged because of an earthquake or flood, your regular home insurance policy might not cover it. You might need to buy separate policies to get protection for those things. It’s a good idea to read your policy carefully and talk to your insurance agent if you have any questions. That way, you can make sure you have the protection you need before something bad happens.

The Role of Home Insurance in Weather-Related Damages

As we discussed different types of damages covered by home insurance companies, now let’s talk about the role of these companies when weather-related damages occur and also what is the process of filing a claim, the role of the insurance adjuster, and how the payout is determined.

Home Insurance & Weather-Related Damage

Home insurance often provides coverage for damage resulting from weather incidents, such as storms, hail, wind, and other acts of nature. The specifics of what is covered will depend on your policy and any exclusions it may have. Standard home insurance policies typically do not cover flood damage, but additional coverage can be purchased through the National Flood Insurance Program.

Filing a Claim

Understanding the process of filing a claim is essential if you want to ensure a smooth and successful outcome. Therefore, it is crucial to familiarize yourself with the steps involved in this process.

When your home suffers weather-related damage, it’s important to contact your insurance company promptly. The process usually involves the following steps:

- Assess and Secure the Property: Before starting the claims process, it’s important to evaluate the damage and take measures to secure the property.

- Review Your Policy: It’s crucial to understand your home insurance policy and any specific requirements for filing a claim.

- Notify Your Insurer: Inform your insurance provider as soon as possible to expedite the claims process.

- Collect Documentation and Evidence: Gather all necessary documentation, including policy details, photos or videos of the damage, and any relevant receipts or invoices.

- Get Repair or Replacement Estimates: If your home needs repairs or replacement of damaged items, get estimates from licensed contractors or professionals.

Role of the Insurance Adjuster

An insurance adjuster, assigned by your insurer, will assess the damage and validate your claim. They inspect the damage, estimate the cost of repairs, and work on behalf of your insurance company. They’ll explain the claims process, review the damage to your home, and ask whether you’ve hired a contractor to fix the damage.

Determining the Payout

The payout is based on the adjuster’s findings and the terms of your insurance policy. The insurance company will either provide a replacement cost, which covers the costs to rebuild your home or repair damages using similar materials, or an actual cash value, which covers the repair or rebuild costs based on the value of your home, taking into account its age and condition. The insurance company typically pays your settlement with a check made out to both you and your mortgage servicer or lender.

Conclusion

In conclusion, home insurance is a valuable investment that protects your home and belongings from a variety of weather-related damages. Whether it’s wind damage, hail damage, snow damage, water damage, or damage from falling objects, a good home insurance policy can provide you with the necessary coverage. However, it’s important to carefully review your policy and understand what is covered and what isn’t. In addition, it’s always a good idea to consult with your insurance agent to ensure that you have the right coverage for your specific needs. With the right home insurance policy, you can have peace of mind knowing that your home and belongings are protected, even when the weather gets rough.